Regional Management (RM)

Long runway for growth, cash generative, and trading at an attractive valuation

This is a shorter, more informal write-up just because I don’t have too much to say about it. The company is Regional Management RM 0.00%↑ and they operate in the consumer finance space, primarily lending to subprime borrowers through company branches and to a lesser extent, online.

Subprime lenders have tightened lending standards since late 2021/2022 when inflation and a slowing economy began to impact low-income borrowers and net charge-offs began to rise across the industry. Today, despite the already tightened credit box, investors are likely cautious about the industry due to: 1) an uncertain economic environment, 2) increased competition with more online lenders and private credit entering the space, and 3) regulatory concerns.

At the moment, I think the most pressing concern is the economic environment. Pre-provision earnings (earnings before the CECL-required provision for credit losses but after actual credit losses) are very sensitive to the economic environment. I would ideally want to start buying a stock like RM at the depths of a recession just as LEIs start to turn positive, when demand for loans are high and net credit losses begin to improve. While that is not the case at the moment, net charge offs have improved and stabilized. The risk of economic deterioration is there but based on delinquency/charge off data, and commentary from companies that operate in the credit space it seems like things will hold up for the next quarter or two.

RM is trading at around 5.5x my estimate of 2025 pre-provision earnings of $5.7 if the economic environment remains stable and anywhere from 2-4x a very rough estimate of normalized pre-provision earnings. At 6-8x 2025 pre-provision earnings, RM is a $34-$45 stock. In a more normalized environment, I believe pre-provision earnings could be $10.7 and with a 6-8x multiple, the stock is $65-85.

These are low multiples but companies in this space have always traded at relatively low multiples. I assume this is due to regulatory concerns and how sensitive the business is to the economic environment. From what I understand, I think businesses in this space that are well-run are higher quality than these multiples give them credit for, but I don’t want to go against historical trends and assume meaningful multiple expansion, especially because RM is a relatively illiquid, micro cap. The multiple may expand as the company scales but this would take some time.

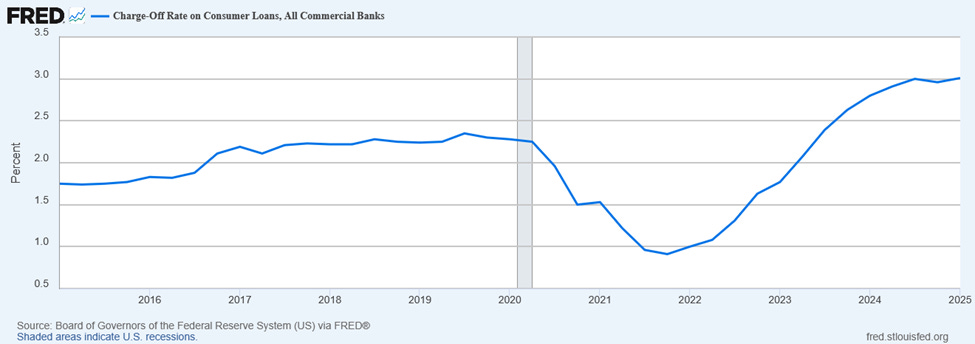

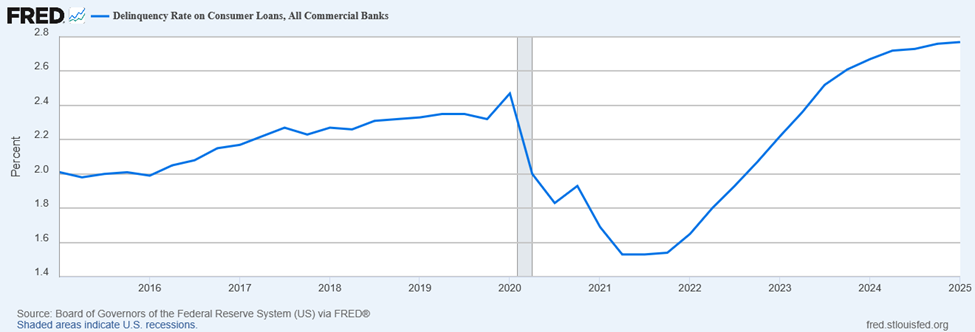

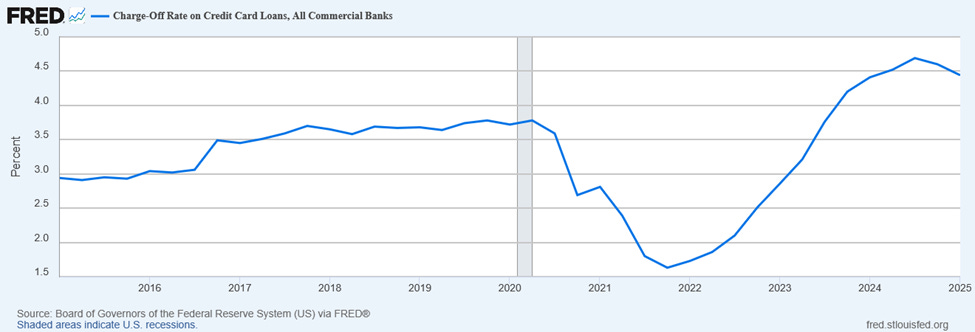

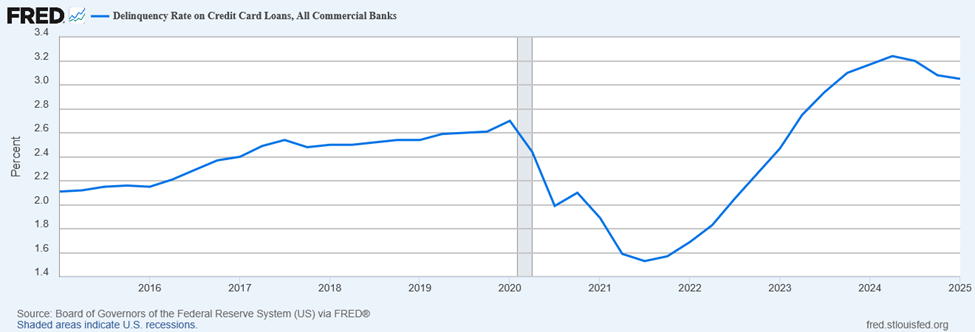

Recent Credit Trends

The following graphs show that delinquencies and charge offs on consumer loans and credit cards have stabilized:

The fact that these are all above pre-pandemic levels gives me some confidence that they won’t spike much higher now that credit boxes have tightened. Additionally, credit card delinquencies and charge offs tend to lead those for consumer loans so the consumer loan charge off/delinquency trends should soon start to move from stabilization to improvement.

Commentary from banks that recently reported earnings also indicates that recent delinquency trends are stable and in line with expectations. If these trends continue, RM should be able to grow pre-provision earnings given their growth in finance receivables.

On the other hand, LEIs continue to point to economic weakness and residential/multifamily construction employment is a particular worry. RM branches are more concentrated in southern states with faster rising housing inventory which may lead to higher construction unemployment in those states. I plan on keeping a close eye on economic data as it rolls in over the next few quarters and will be fast to cut RM on signs that conditions are deteriorating.

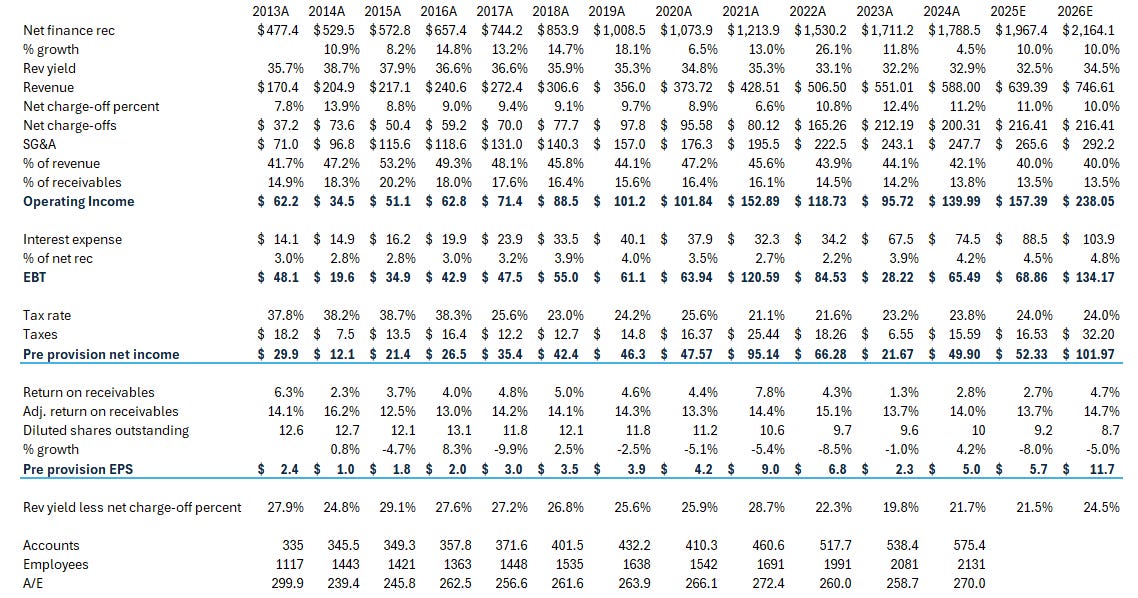

Valuation

I think that pre-provision earnings seems to be the most accurate representation of the economic reality of businesses in this industry. Below is a rough model that shows how I’m thinking about RM’s financials. 2026E shows my estimate of normalized earnings, but I’m not putting much weight on the precise number or the year that will happen. What makes this figure normalized is my assumption of a 34.5% revenue yield on net finance receivables, and net charge-offs equal to 10% of net finance receivables. Both figures are based loosely on historical metrics and management’s guidance from the Q3 2023 earnings call that “over the long run, under a normal economic environment, we continue to expect that our net [charge off] rate will be in the range of 8.5% to 9% based on our current product mix and underwriting”.

The main idea is that the business has a long runway for growth, is cash generative, and the stock is trading at an attractive valuation at a time when the economic environment has already slowed. This means that receivables will grow, the company will return cash to shareholders, and at some point, there will be revenue yield, margin, and multiple expansion as the economy normalizes to a more benign state. At that point the stock could trade at 6-8x pre-provision EPS of $10.7, or $65-85. In the meantime, if economic conditions remain relatively stable over the next few quarters, the stock could trade at 6-7x pre-provision EPS of $5.7, or $34-$40.